At an annual growth of 4.4%, Airbus anticipates demand for 37,400 new passenger and dedicated freight aircraft and values the market at about $5.8 trillion over the next 20 years. Coupled with the decline in the hub and spoke network of commercial aviation and a rise in point to point network, narrowbody (single-aisle) airliners could take up more than 70% of this market share. So it is would only be logical to expect some cut-throat competition in this segment. With the Bombardier C-series, Embraer E-jet, Comac C919, Sukhoi Superjet, Airbus A-320 and Boeing 737 the competition, at least on paper, looks pretty stiff too. The ground reality, however, begs to differ. It is no secret that the aerospace industry for long has been controlled by a few wealthy nations and their corporations and the commercial aviation market is dominated by the duopoly of Airbus and Boeing. However, with rising demands and increasing reach of aviation, there were glimmers of hope for a more inclusive industry, but the recent trend of mergers and acquisitions has ushered in a new era of market consolidation and made it even more exclusive. To understand more about it let us take a look at how the aerospace industry is moving towards oligarchy and the impact it could have in the long run.

Airlines and MROs-

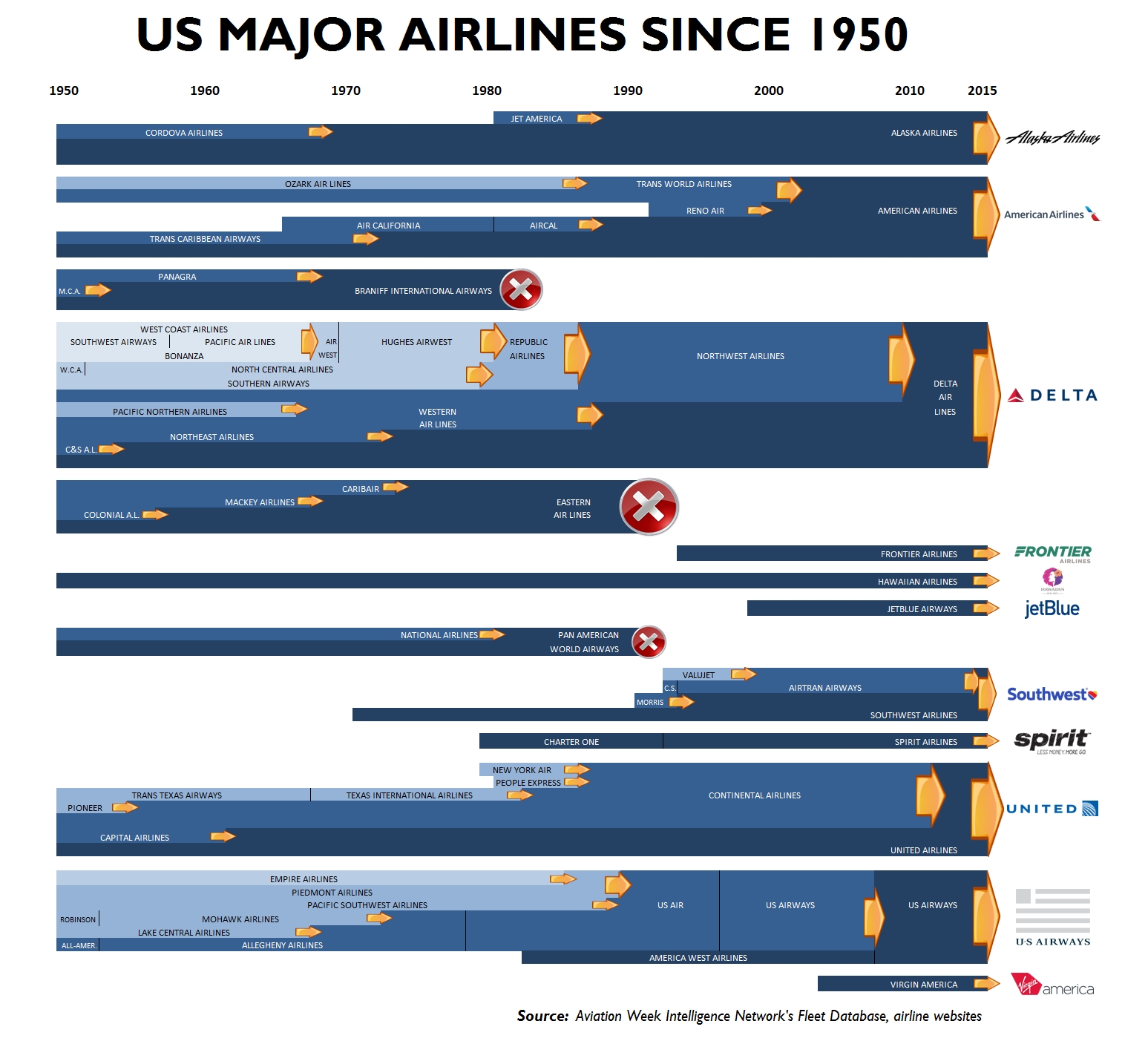

Did you know that Swiss Air, Austrian Airlines, Brussels Airlines, Eurowings and Lufthansa are all owned and controlled by the Lufthansa group? Or that Air France and KLM are owned by the same holding company? The above image gives us a fair amount of idea on how the airline industry in the US has shaped up over the years and given below is an idea of how things might pan out in Europe.

The Airlines say that M&A help them improve overall flight experience and reduce cost. But how much of the cost benefit is transferred to the customers’ is pretty questionable. Since 2014 the price of jet fuel (one of the biggest cost for airlines) has fallen drastically, this, in turn, has triggered a fare war amongst European airline but the prices in America have more or less stayed the same. Through market consolidation, American airlines have reduced competition and earned ($ 22.40) 3 times more money per passenger than there European($7.84) counterparts.

Coming to flight experience, we all know of the bloody battles (quite literally) passengers have to fight just to stay on board. From getting punched in the face to being thrown out with your family, flying indeed has never been this exciting. We can clearly see that M&A hasn’t really helped the customers and their adverse effect though are also being felt by the supporting industry.

Take for example the MRO industry. Thanks to more efficient and advanced aircraft the past decade has seen an unprecedented consolidation of the MRO industry. Killing any new vacancies that might be created due to the growth of the sector. Hoping to gain for the economies of scale from these mega airlines MROs failed to foresee the growing interest of OEMs in the lucrative after-sales market. OEMs which have access to critical documents and OEMs which have already started to restrict third-party access to engineering data and repair manuals for new-generation equipment. With aircrafts getting more and more connected, they generate huge amounts of data and even predict maintenance requirements on their own. Data which could potentially change the face of the MRO industry and debates on who gets access to these data has already started. With the CTO of Wizz Air Heiko Holm going on record to state that – The OEMs have taken over the aftermarket, and we do not support it- we can’t help but wonder what the future holds.

Defence Mergers-

The aerospace and defence industry go hand in and what happens to one is bound to affect the other. With the number of prime contractors in the American defence sector effectively cut from 20 to just 6, and these 6 often forming joint teams to bid on Department of Defense (DoD) programmes. It is no surprise that the then U.S. Defense Secretary Ash Carter was not too pleased when Lockheed Martin acquired Sikorsky Aircraft at a cost of about $ 9 billion. It would be defamatory to suggest that defence contractors lack innovation, but with non-traditional companies such as Apple and Dell accounting for around 35% of the Pentagon’s spend on procurement and services, and with former deputy Secretary of Defence William Lynn III clearly stating that commercial technology now far exceeds what the defence sector can produce in many fields. We can’t help but wonder about the role of lack of competition in it. Take for example the American LSR-B (Long Range Strike Bomber) program, where two supposed arch rivals Boeing and Lockheed Martin teamed up and lost to a design by Northrop Grumman (B-21 Raider) which has an eerie resemblance to its much older cousin the B-2 sprit Bomber. Such team-ups not only brings the factor of size is power into the equation but also makes it very difficult to run a proper selection process and potentially reduces competitive incentives on pricing and delivery – precisely the problems which have repeatedly beset US arms programmes over recent decades. No wonder the Pentagon is not too pleased with the prospect of further consolidation of the industry. The same worrying trend is also visible in the commercial aircraft market as well.

Commercial Aviation-

With $72 billion spent on aerospace and defence M&A globally in 2017, it has been the highest in recorded history. While the number of deals taking place has stayed more or less constant as compared to 2016 the average deal size has increased by 69%. Major buyouts like Safran taking over Zodiac or talks of blockbuster mergers like UTC/Rockwell are becoming more and more common. Creation of these one-stop shop for aircraft manufacturers and airlines have made it extremely difficult for new companies to come up and flourish in this domain. Take for example the C-series by Bombardier an aircraft that is much more superior in terms of performance and passenger comfort when compared to the aircraft the Boeing/Airbus duopoly has to offer. However, thanks to the duopoly of these manufacturers no airlines are willing to buy the C-series and when Delta announced its plan to buy 75 CS-100, Boeing threatened to slap a 292% tariff on the aircraft. What happened ultimately? well, the C- series is now owned by Airbus and CS-100/300 have become A220-100/300 and Boeing is in talks to take over Embraer’s commercial aircraft division. Conveniently wiping out the competition. What about the Sukhoi Superjet and Comac C919? Well, Russian jets have never really made a mark outside of Russia and interjet one of the largest operators of the jet was forced to cannibalize grounded Superjets due to lack of spare and support. Similarly, the C919 thanks to Trump’s trade war could fill order books through domestic airlines the recent mergers spell doom for its international ambitions. Making the Airbus/Boeing Duopoly stronger than ever. Coupled with rising costs of developing new aircraft and the extensive web of multinational suppliers the duopoly has created, it is highly unlikely that we would see the emergence of a successful jetliner outside of the duopoly.

Final Word-

While it is next to impossible to have another East India company in the making, one can never be too cautious of the impact such giants can have. Employing thousands of people and generating billions in revenue they already have the power to shape government policies, demand tax breaks and other benefits from their hosts. It wouldn’t be surprising if such power leads to some nasty outcomes in the future. Hopefully, such a day would never arrive, hope though is not the only thing we should be banking on.

Probably all the bright brains today are specialising in M&A rather than aerospace R&D. This kind of ‘consolidation’ and oligarchy is increasingly becoming the norm in even the technology and innovation space with few giants like Amazon, Google, Facebook etc dominating the internet-enabled businesses. And here in India, we haven’t even started. At least in A&D, we have to be cautious we don’t let in another East India Company in through the door. Good analysis, Jetboy. Keep it up.